Ridge & Lasso Regression in R — Penalized Linear Models with glmnet

Ridge & Lasso Regression (Penalized OLS)

Why penalization?

OLS estimates can become unstable when:

- predictors are highly correlated (multicollinearity),

- the number of predictors is large relative to the sample size,

- you want a model that generalizes better (lower variance) and/or performs variable selection.

Penalized regression adds a constraint/penalty to shrink coefficients toward zero, trading a bit of bias for lower variance.

Theory: Ridge, Lasso, Elastic Net

Assume a linear model \(y = X\beta + \epsilon\) with \(X \in \mathbb{R}^{n \times p}\). The OLS objective minimizes RSS: \[ \min_{\beta_0,\beta}\ \frac{1}{2n}\sum_{i=1}^n (y_i - \beta_0 - x_i^T\beta)^2 \]

Ridge (L2 penalty)

\[ \min_{\beta_0,\beta}\ \frac{1}{2n}\sum_{i=1}^n (y_i - \beta_0 - x_i^T\beta)^2\ +\ \lambda \sum_{j=1}^p \beta_j^2 \]

- Shrinks coefficients smoothly.

- Typically does not set coefficients exactly to zero (no hard feature selection).

- Very useful under multicollinearity.

Lasso (L1 penalty)

\[ \min_{\beta_0,\beta}\ \frac{1}{2n}\sum_{i=1}^n (y_i - \beta_0 - x_i^T\beta)^2\ +\ \lambda \sum_{j=1}^p |\beta_j| \]

- Encourages sparsity: some \(\hat\beta_j = 0\).

- Performs variable selection (often easier interpretation).

Elastic Net (mix L1 + L2)

Elastic Net combines both: \[ \min_{\beta_0,\beta}\ \frac{1}{2n}\|y-\beta_0\mathbf{1}-X\beta\|_2^2 \ +\ \lambda\left[(1-\alpha)\frac{1}{2}\|\beta\|_2^2 + \alpha\|\beta\|_1\right] \] with \(0 \le \alpha \le 1\):

- \(\alpha = 0\) → ridge

- \(\alpha = 1\) → lasso

- \(0<\alpha<1\) → elastic net

Hyperparameter intuition

- \(\lambda = 0\): no penalization (≈ OLS).

- \(\lambda \uparrow\): stronger shrinkage; lasso sets more coefficients to zero.

- \(\alpha\): controls sparsity vs stability.

Practice in R with glmnet

Key points:

glmnetexpects a numeric matrixx(usemodel.matrix()for factors).- Use cross-validation to select \(\lambda\) via

cv.glmnet(). - Common choices:

lambda.min: minimizes CV error.lambda.1se: simplest model within 1 standard error (more regularization; often more robust).

Example: Ridge vs Lasso on mtcars (Gaussian regression)

We predict mpg using a mix of numeric and categorical

features.

Step 1: Data preparation (design matrix)

library(dplyr)

df <- mtcars |>

mutate(

cyl = factor(cyl),

am = factor(am, labels = c("auto", "manual")),

vs = factor(vs)

)

# Model matrix: adds intercept column by default; glmnet handles intercept separately,

# so we remove it with "-1" here and let glmnet fit intercept = TRUE.

X <- model.matrix(mpg ~ . - 1, data = df)

y <- df$mpg

dim(X)## [1] 32 12## cyl4 cyl6 cyl8 disp hp drat

## Mazda RX4 0 1 0 160 110 3.90

## Mazda RX4 Wag 0 1 0 160 110 3.90

## Datsun 710 1 0 0 108 93 3.85

## Hornet 4 Drive 0 1 0 258 110 3.08

## Hornet Sportabout 0 0 1 360 175 3.15

## Valiant 0 1 0 225 105 2.76Step 2: Train/test split

Step 3: Baseline OLS (for comparison)

train_ols <- data.frame(mpg = y_train, X_train)

test_ols <- data.frame(mpg = y_test, X_test)

fit_ols <- lm(mpg ~ ., data = train_ols)

summary(fit_ols)##

## Call:

## lm(formula = mpg ~ ., data = train_ols)

##

## Residuals:

## Min 1Q Median 3Q Max

## -3.7677 -1.3928 -0.0578 0.7350 4.6582

##

## Coefficients: (1 not defined because of singularities)

## Estimate Std. Error t value Pr(>|t|)

## (Intercept) 16.57753 19.19814 0.863 0.4048

## cyl4 2.46724 6.70666 0.368 0.7194

## cyl6 -0.20269 4.81932 -0.042 0.9671

## cyl8 NA NA NA NA

## disp 0.02219 0.02786 0.797 0.4411

## hp -0.03423 0.04199 -0.815 0.4308

## drat -0.12025 2.31432 -0.052 0.9594

## wt -4.53231 2.54011 -1.784 0.0997 .

## qsec 0.75808 0.95328 0.795 0.4419

## vs1 1.53834 2.93413 0.524 0.6096

## ammanual 2.47468 2.99684 0.826 0.4251

## gear 0.12976 2.20021 0.059 0.9539

## carb 0.64798 1.23947 0.523 0.6106

## ---

## Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

##

## Residual standard error: 3.033 on 12 degrees of freedom

## Multiple R-squared: 0.8818, Adjusted R-squared: 0.7734

## F-statistic: 8.138 on 11 and 12 DF, p-value: 0.0005336pred_ols <- predict(fit_ols, newdata = test_ols)

rmse <- function(y, yhat) sqrt(mean((y - yhat)^2))

rmse_ols <- rmse(y_test, pred_ols)

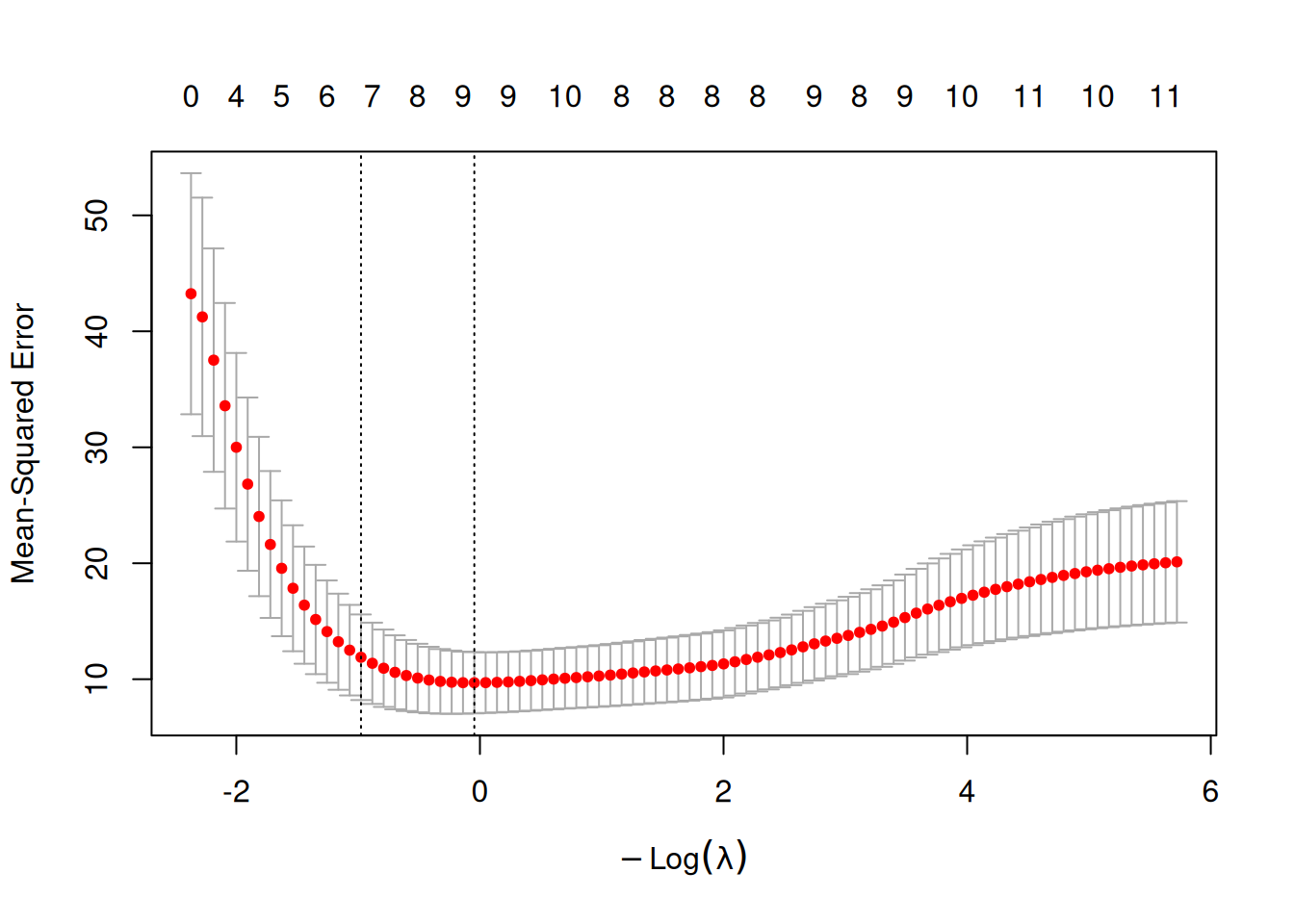

rmse_ols## [1] 2.1292Step 4: Ridge regression (alpha = 0) with CV

# install.packages("glmnet") # if needed

library(glmnet)

set.seed(123)

cv_ridge <- cv.glmnet(

x = X_train,

y = y_train,

alpha = 0, # ridge

nfolds = 10, # default is 10

standardize = TRUE

)

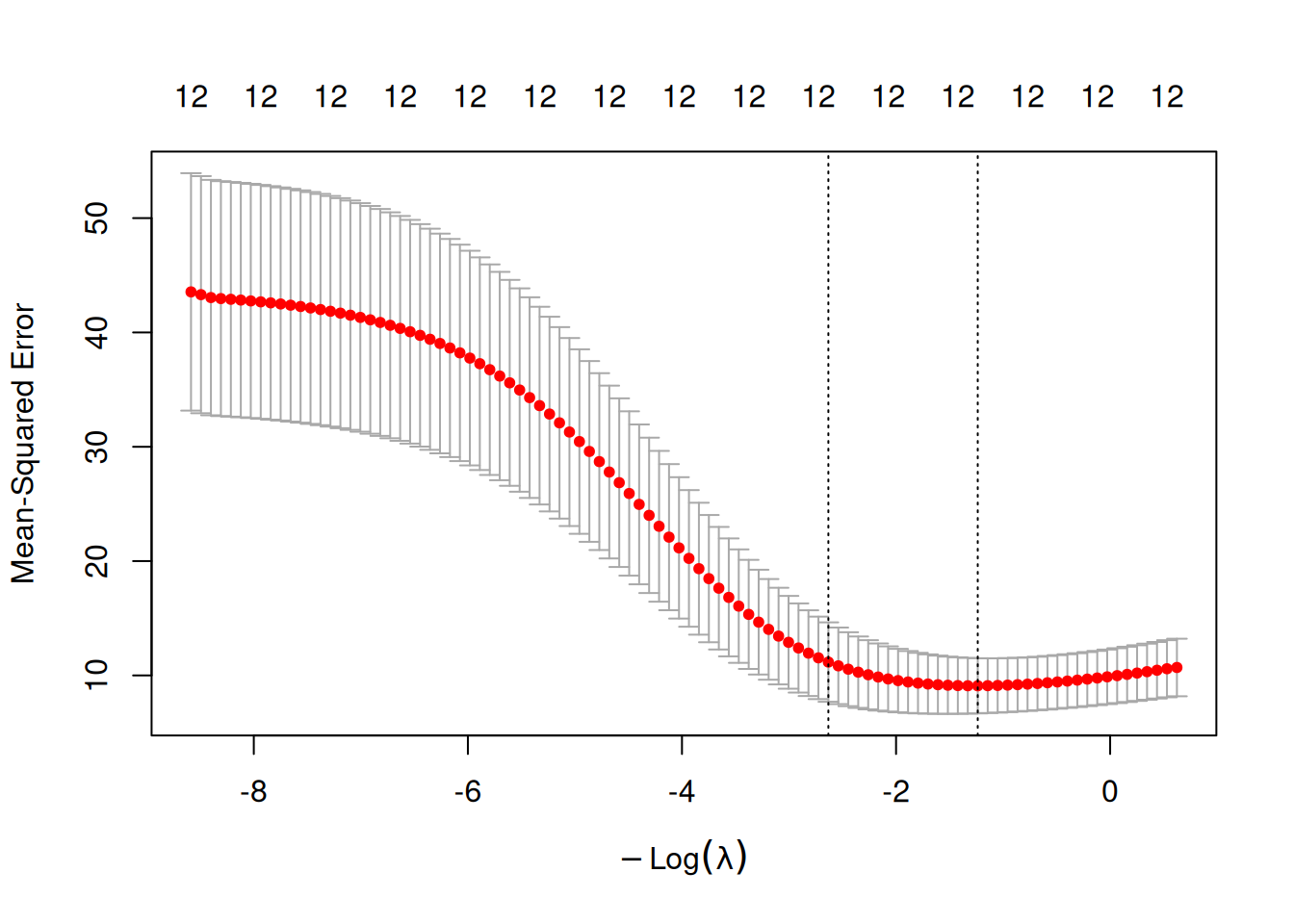

plot(cv_ridge)

## [1] 3.444694## [1] 13.90629Fit ridge at selected lambda and evaluate:

pred_ridge_min <- predict(cv_ridge, newx = X_test, s = "lambda.min")

pred_ridge_1se <- predict(cv_ridge, newx = X_test, s = "lambda.1se")

rmse_ridge_min <- rmse(y_test, pred_ridge_min)

rmse_ridge_1se <- rmse(y_test, pred_ridge_1se)

c(rmse_ols = rmse_ols, rmse_ridge_min = rmse_ridge_min, rmse_ridge_1se = rmse_ridge_1se)## rmse_ols rmse_ridge_min rmse_ridge_1se

## 2.129200 2.055639 2.218518Inspect coefficients:

## 10 x 1 sparse Matrix of class "dgCMatrix"

## lambda.min

## (Intercept) 20.049804674

## cyl4 1.509365191

## cyl6 -0.715565529

## cyl8 -1.064064671

## disp -0.005891425

## hp -0.010170279

## drat 0.913128419

## wt -1.233903891

## qsec 0.153282689

## vs1 1.011905504Step 5: Lasso regression (alpha = 1) with CV

set.seed(123)

cv_lasso <- cv.glmnet(

x = X_train,

y = y_train,

alpha = 1, # lasso

nfolds = 10,

standardize = TRUE

)

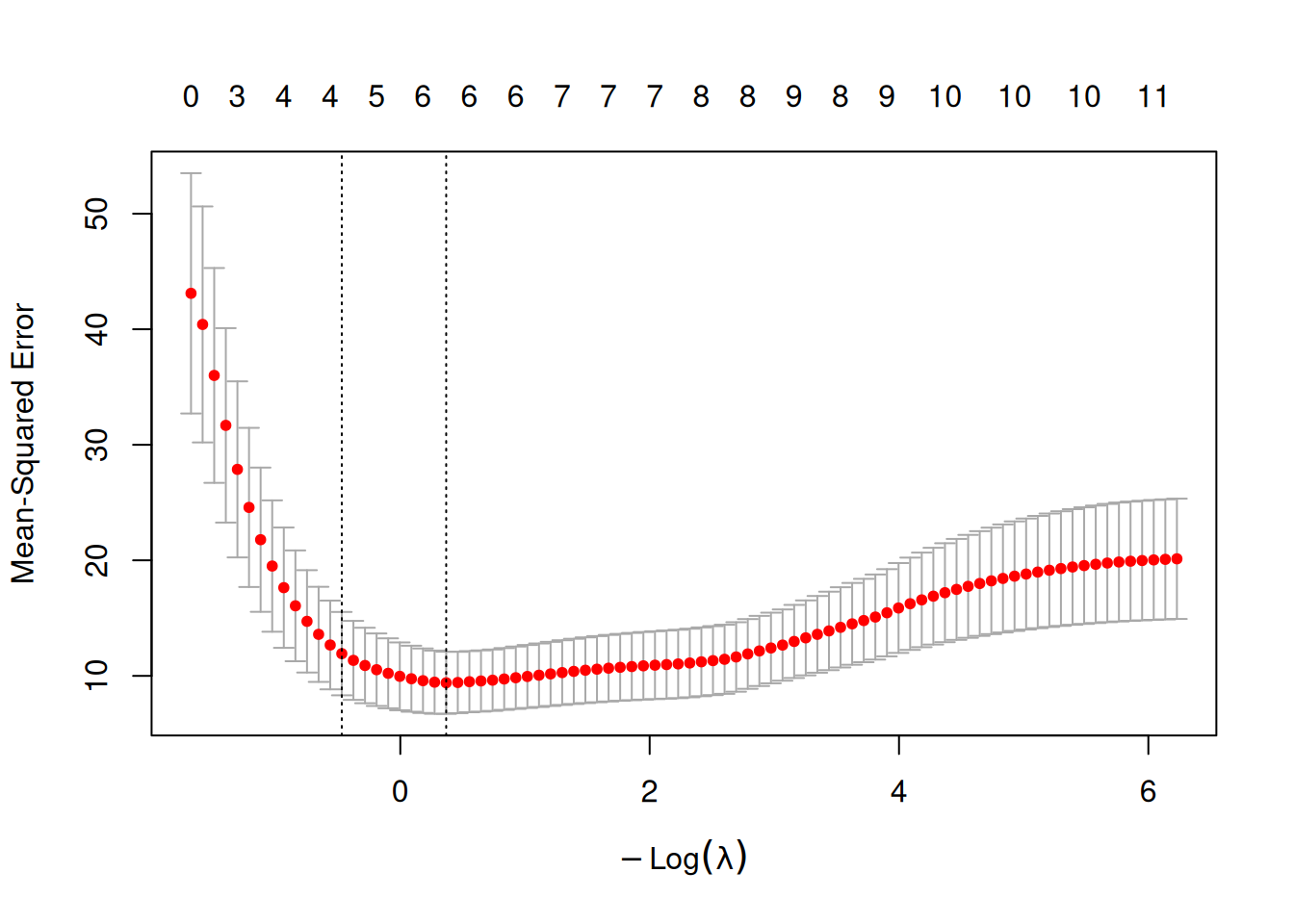

plot(cv_lasso)

## [1] 0.6921193## [1] 1.598885Evaluate and compare:

pred_lasso_min <- predict(cv_lasso, newx = X_test, s = "lambda.min")

pred_lasso_1se <- predict(cv_lasso, newx = X_test, s = "lambda.1se")

rmse_lasso_min <- rmse(y_test, pred_lasso_min)

rmse_lasso_1se <- rmse(y_test, pred_lasso_1se)

c(

rmse_ols = rmse_ols,

rmse_lasso_min = rmse_lasso_min,

rmse_lasso_1se = rmse_lasso_1se

)## rmse_ols rmse_lasso_min rmse_lasso_1se

## 2.129200 2.060473 2.171117Check sparsity (number of non-zero coefficients):

## [1] 6List selected predictors:

## [1] "(Intercept)" "cyl4" "cyl8" "hp" "wt"

## [6] "vs1"Step 6: Coefficient paths (optional)

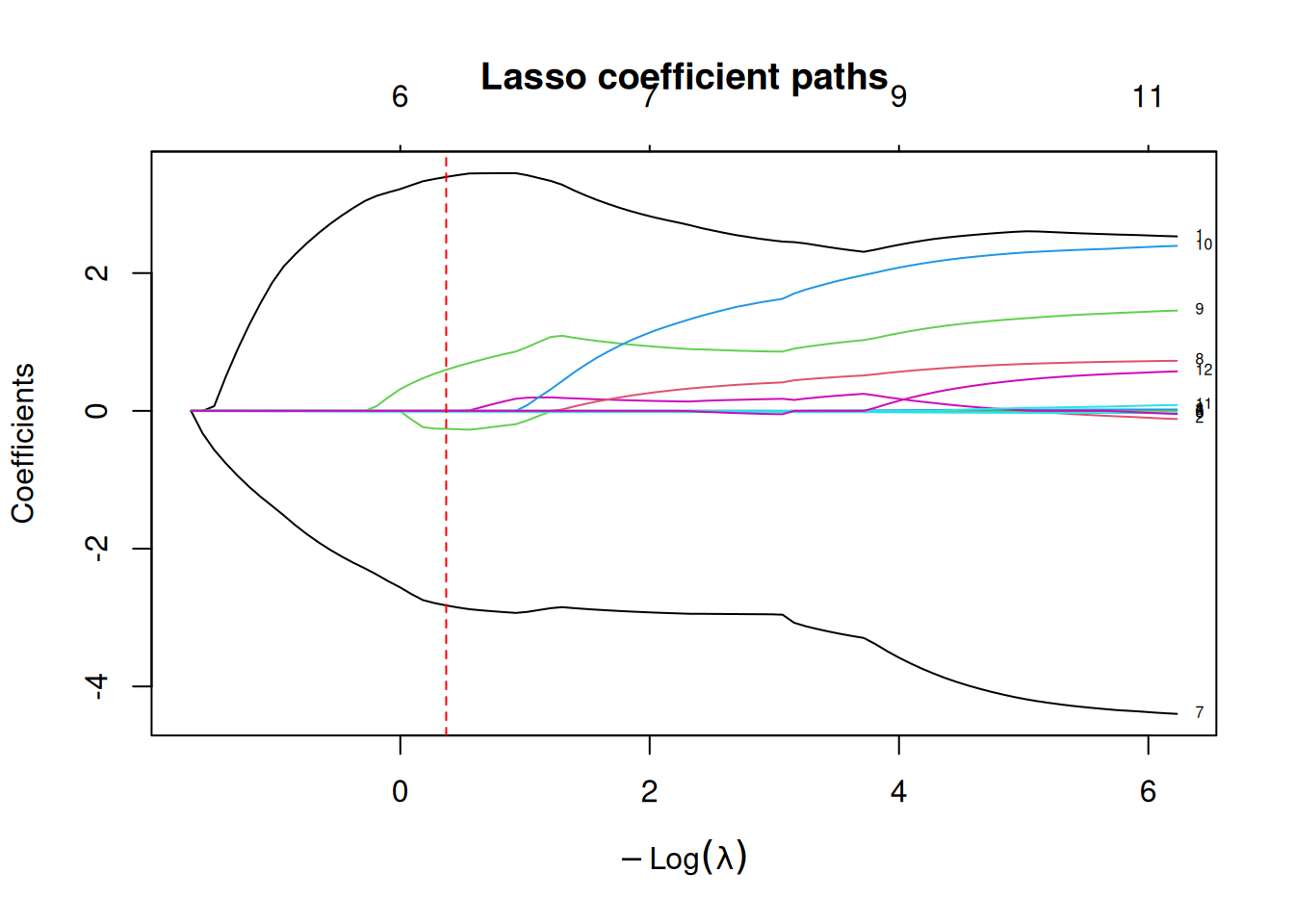

fit_lasso_path <- glmnet(X_train, y_train, alpha = 1, standardize = TRUE)

plot(fit_lasso_path, xvar = "lambda", label = TRUE, main = "Lasso coefficient paths")

abline(v = -log(cv_lasso$lambda.min), lty = 2, col = "red")

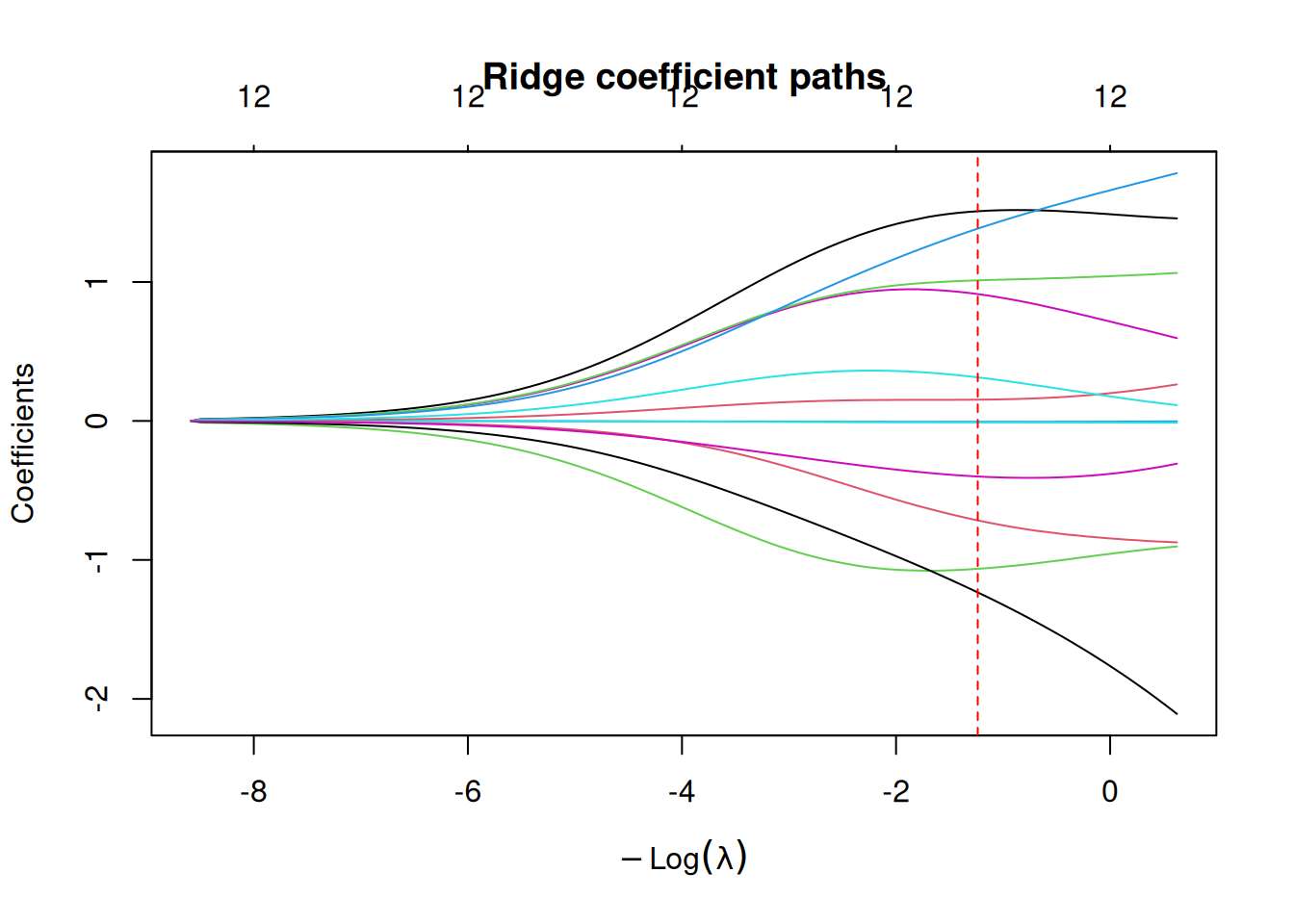

fit_ridge_path <- glmnet(X_train, y_train, alpha = 0, standardize = TRUE)

plot(fit_ridge_path, xvar = "lambda", label = FALSE, main = "Ridge coefficient paths")

abline(v = -log(cv_ridge$lambda.min), lty = 2, col = "red")

Optional: Elastic Net (alpha between 0 and 1)

If predictors are highly correlated, elastic net can outperform pure lasso.

set.seed(123)

cv_enet <- cv.glmnet(

x = X_train,

y = y_train,

alpha = 0.5, # elastic net

nfolds = 10,

standardize = TRUE

)

plot(cv_enet)

pred_enet <- predict(cv_enet, newx = X_test, s = "lambda.min")

rmse_enet <- rmse(y_test, pred_enet)

c(rmse_lasso_min = rmse_lasso_min, rmse_ridge_min = rmse_ridge_min, rmse_enet_min = rmse_enet)## rmse_lasso_min rmse_ridge_min rmse_enet_min

## 2.060473 2.055639 2.077020Best practices & warnings

- Always use cross-validation for \(\lambda\); prefer

lambda.minwhen you want stability and parsimony. - Standardization is important so that the penalty treats predictors comparably.

- Lasso can be unstable when predictors are strongly correlated (it may pick one arbitrarily); elastic net is often safer.

- If the goal is inference (p-values, CI), penalized regression needs extra care (post-selection inference); treat as predictive by default.

Summary

You learned how to: - Define ridge/lasso/elastic net with penalized

objectives. - Fit ridge and lasso in R using glmnet +

cv.glmnet(). - Select \(\lambda\) via CV (lambda.min

vs lambda.1se). - Compare test RMSE and interpret shrinkage

vs sparsity.

Penalized regression is a modern alternative to stepwise selection for regression problems with many correlated predictors.

A work by Gianluca Sottile

gianluca.sottile@unipa.it